Unified Payments Interface (UPI) has revolutionized the way people handle transactions, making payments fast, seamless, and highly secure.

As one of the most successful digital payment systems, UPI has already processed billions of transactions, cementing its position as a game-changer in the fintech world.

But is building a UPI app worth your investment? Absolutely.

With its unparalleled adoption rate and integration capabilities, UPI apps are no longer limited to India – they’re setting a global standard.

If you’re wondering whether developing a UPI app is the right move for your business, you’re in the right place.

This guide dives deep into everything you need to know about UPI app development, from understanding its ecosystem to outlining its development process.

Whether you’re an entrepreneur, fintech enthusiast, or tech leader, this blog will equip you with the insights to build a robust and scalable UPI app that meets user demands.

Let’s explore the potential of UPI apps and uncover how they can elevate your business.

Statistics: Why UPI Apps Are the Future of Payments

To understand the growing prominence of UPI apps, let’s take a look at some compelling statistics:

- UPI transaction volume crossed 12 billion in December 2024, demonstrating a 30% year-on-year growth.

- UPI accounts for over 75% of all digital transactions in India, showcasing its dominance in the fintech ecosystem.

- Average transaction value per UPI payment has steadily increased to ₹2,500, highlighting its growing usage for high-value payments.

- International UPI adoption has begun in countries like Singapore and the UAE, enabling cross-border transactions.

- Over 10 million merchants have integrated UPI payment systems into their businesses.

- By 2030, UPI is projected to contribute 5% to India’s GDP, solidifying its economic impact.

- UPI-based credit transactions surged by 40% in 2024, indicating its potential for expanded financial services.

- Peer-to-peer transactions via UPI grew by 25% in 2024, showing its popularity among individual users.

- Over 1,000 banks are now part of the UPI network, offering unparalleled connectivity.

- UPI is now recognized as the most secure payment method, with advanced encryption standards and two-factor authentication.

These figures illustrate that UPI is not just a payment method – it’s a thriving ecosystem poised for global expansion. Ready to leverage this technology?

Let’s delve deeper into what makes a UPI app unique.

What is a UPI App?

A UPI app is a digital payment solution that enables seamless and instant money transfers between bank accounts through a smartphone.

Built on the Unified Payments Interface (UPI) system, these apps facilitate transactions without requiring additional banking details like account numbers or IFSC codes.

With just a mobile number or UPI ID, users can make payments, request money, and even pay bills with ease.

The system is managed by the National Payments Corporation of India (NPCI) and is renowned for its interoperability, meaning users can transact across different banks and apps.

Additionally, UPI apps integrate advanced security protocols, including two-factor authentication and real-time fraud detection, making them reliable and secure for users.

For businesses, developing a UPI app provides opportunities to tap into the thriving digital payment market.

Whether you’re looking to create a UPI app for retail, e-commerce, or financial services, the potential to attract millions of users is immense.

In this UPI app development guide, we’ll uncover everything you need to know to successfully build and launch your app.

Is UPI Payment Limited to India?

While Unified Payments Interface (UPI) originated in India and gained rapid adoption across the country, its impact is no longer confined to Indian borders.

Initially introduced by the National Payments Corporation of India (NPCI), UPI was designed to streamline digital payments and make financial transactions accessible to everyone.

Today, UPI is expanding its footprint globally:

- International Collaborations: Countries like Singapore, UAE, and Bhutan have started integrating UPI into their payment systems, enabling seamless cross-border transactions. This expansion is part of NPCI’s initiative to position UPI as a global payment system.

- Ease of Cross-Border Transactions: With its integration into platforms like PayNow (in Singapore), UPI simplifies international remittances, offering users a faster and cheaper alternative.

- Growing Interest from Global Markets: Several countries are exploring partnerships to replicate UPI’s model, given its efficiency and scalability.

This widespread interest makes it clear: while UPI started as an Indian innovation, it is evolving into a global payment standard.

For businesses, investing in UPI app development is no longer just about targeting Indian users – it’s about tapping into a growing international market.

Wondering how this payment ecosystem works? Let’s break it down.

Understanding the UPI Payment Ecosystem: A Comprehensive Breakdown

The UPI payment ecosystem is a seamless and highly interconnected network that powers digital transactions across individuals, businesses, and banks.

Its streamlined infrastructure ensures secure, instant, and reliable payments, making it a cornerstone of modern financial technology.

Let’s dive into the critical components that define this system:

1. Banks as PSPs (Payment Service Providers)

Banks form the foundation of the UPI ecosystem, enabling transactions between accounts in real time.

They play two primary roles:

- Issuer Bank: The bank holding the payer’s account ensures that funds are deducted securely.

- Acquirer Bank: The bank associated with the payee ensures funds are credited instantly.

Each bank involved in the UPI ecosystem is integrated through NPCI’s platform, ensuring interoperability and security.

Moreover, users can link multiple bank accounts to a single UPI ID, making transactions simpler and more efficient.

The National Payments Corporation of India (NPCI) oversees the technical and operational backbone of UPI. It ensures:

- Real-Time Processing: Managing billions of transactions daily with minimal latency.

- Interoperability: Allowing users to transact seamlessly between different banks and UPI platforms.

- Security Protocols: Utilizing encryption and two-factor authentication to safeguard transactions.

The NPCI also facilitates innovations such as recurring mandates, UPI AutoPay, and cross-border payment integrations, further enhancing the system’s capabilities.

3. Merchants and Businesses

Merchants are significant stakeholders in the UPI ecosystem.

By integrating UPI into their payment systems, they:

- Enable payments through QR codes, UPI IDs, or mobile numbers.

- Benefit from Zero MDR (Merchant Discount Rate), which reduces costs and encourages small businesses to adopt digital payments.

- Improve customer experiences with faster checkouts and seamless payment confirmations.

UPI’s ease of use and affordability have made it a preferred choice for e-commerce, retail, and service-based businesses.

4. Users: The Core of the Ecosystem

For users, UPI simplifies payments by eliminating the need for traditional banking details like account numbers or IFSC codes.

They benefit from:

- Single Interface: Linking multiple bank accounts to a single UPI ID.

- Ease of Access: Performing transactions with just a mobile number, UPI ID, or QR code.

- Universal Usability: UPI apps are compatible across banks and service providers, giving users the flexibility to choose their preferred app.

This simplicity has driven mass adoption, with millions of people using UPI for everyday transactions.

5. Third-Party UPI Apps: Driving Adoption

Apps like Google Pay, PhonePe, Paytm, and others play a crucial role in UPI’s success.

They act as the user interface for the ecosystem, offering features such as:

- Rewards and Cashback: Attracting users through loyalty programs.

- Bill Payments and Subscriptions: Integrating value-added services for convenience.

- Secure Authentication: Implementing biometric verification, PINs, and encryption.

These third-party apps have democratized access to UPI by making it user-friendly, visually appealing, and accessible even to non-tech-savvy individuals.

6. Cross-Border Payments: Expanding Horizons

UPI’s integration into international payment systems, like Singapore’s PayNow, has expanded its reach beyond Indian borders.

Features include:

- Affordable Remittances: Providing a low-cost alternative for cross-border payments.

- Instant Transfers: Reducing delays typical in traditional international transactions.

- Interoperability with Global Standards: Enabling seamless transactions across countries adopting the system.

7. Regulatory Oversight

The Reserve Bank of India (RBI) provides regulatory guidance to ensure UPI remains safe, efficient, and scalable.

Compliance with banking norms, data privacy laws, and anti-money laundering measures ensures the ecosystem’s integrity.

The UPI payment ecosystem exemplifies how technology, banking, and user-centric design can revolutionize financial transactions.

For businesses looking to create a UPI app, understanding this robust framework is critical to delivering a seamless and feature-rich solution.

How is UPI Payment Different from Payment Systems Across the World?

The Unified Payments Interface (UPI) stands apart from other global payment systems by offering a unique combination of features, affordability, and accessibility.

The table below compares UPI with other popular payment systems like PayPal, Venmo, and Alipay, highlighting its strengths:

| Feature | UPI | Global Systems (PayPal, Venmo, Alipay, etc.) |

| Interoperability | Seamless transactions between different banks and apps (e.g., PhonePe to Google Pay). | Often restricted to users on the same platform, limiting flexibility. |

| Merchant Costs (MDR) | Zero MDR policy encourages adoption among small merchants. | Charges significant MDR, making it costly for businesses. |

| Transaction Costs | Free or negligible transaction fees for users. | High fees, especially for cross-border payments. |

| Settlement Time | Instant fund transfer and settlement. | Delayed settlements ranging from hours to days. |

| Security | Two-factor authentication with UPI PIN and bank-level encryption. | Strong security, but often lacks bank-integrated two-factor authentication. |

| Accessibility | Works on smartphones, feature phones (via USSD), and offline modes. | Limited to smartphones or specific devices. |

| Scalability | Handles billions of transactions monthly without disruptions. | Regional or industry-specific, with limited scalability. |

| Multi-Functionality | Single platform for money transfers, bill payments, subscriptions, and loans. | Often specialized, requiring multiple platforms for different services. |

| Global Reach | Expanding internationally (e.g., Singapore, UAE integration). | Limited availability in certain regions; cross-border payments can be complex. |

This comparison underscores how UPI has revolutionized the payment landscape by combining affordability, inclusivity, and functionality.

For businesses looking to build a UPI app, these advantages make it a highly competitive option in the global market.

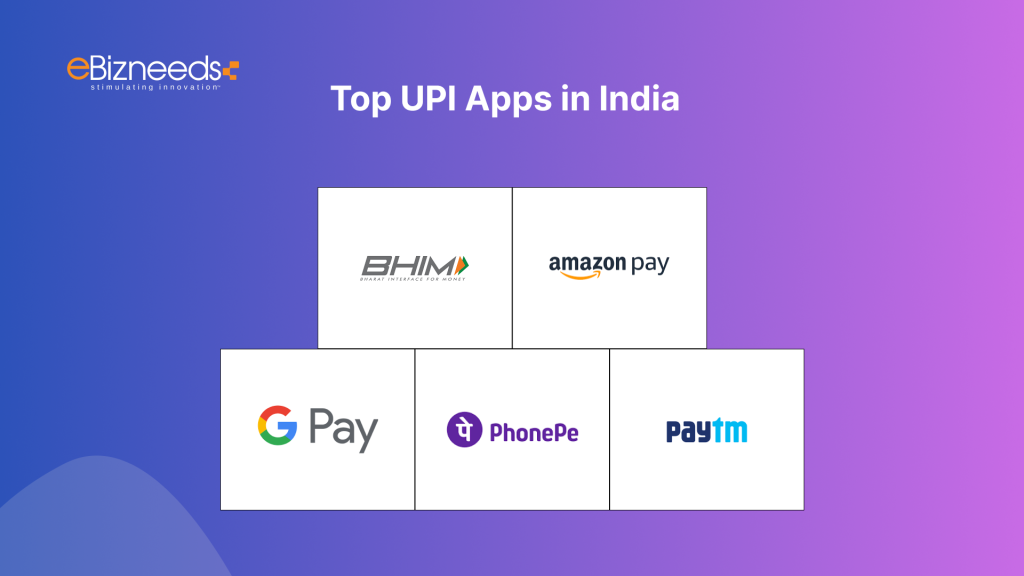

Top UPI Apps in India and Around the World

Unified Payments Interface (UPI) has revolutionized digital transactions, with several apps gaining immense popularity for their features, reliability, and ease of use.

Here’s a look at the top UPI apps in India and those with similar functionalities outside India:

Top UPI Apps in India

1. Google Pay (GPay)

One of the most widely used UPI apps in India, offering seamless money transfers, bill payments, and rewards.

- Key Features: Bank account linking, QR code payments, and UPI ID-based transactions.

- USP: User-friendly interface and global brand trust.

2. PhonePe

A dominant player in the Indian UPI ecosystem, enabling instant money transfers and merchant payments.

- Key Features: Wallet services, mutual fund investments, and insurance purchases.

- USP: Extensive merchant network and integrated financial services.

3. Paytm

Initially a wallet-based app, Paytm has integrated UPI to offer seamless payments and a wide array of services.

- Key Features: Utility bill payments, mobile recharges, and in-app shopping.

- USP: All-in-one platform combining e-commerce and payments.

4. BHIM App

The official UPI app launched by the National Payments Corporation of India (NPCI).

- Key Features: Secure, fast transactions directly from bank accounts.

- USP: Minimalistic design and government backing.

5. Amazon Pay UPI

Amazon’s entry into the UPI space, allowing users to make payments and earn cashback within the app.

- Key Features: Shopping payments, bill payments, and rewards.

- USP: Integration with Amazon’s e-commerce platform.

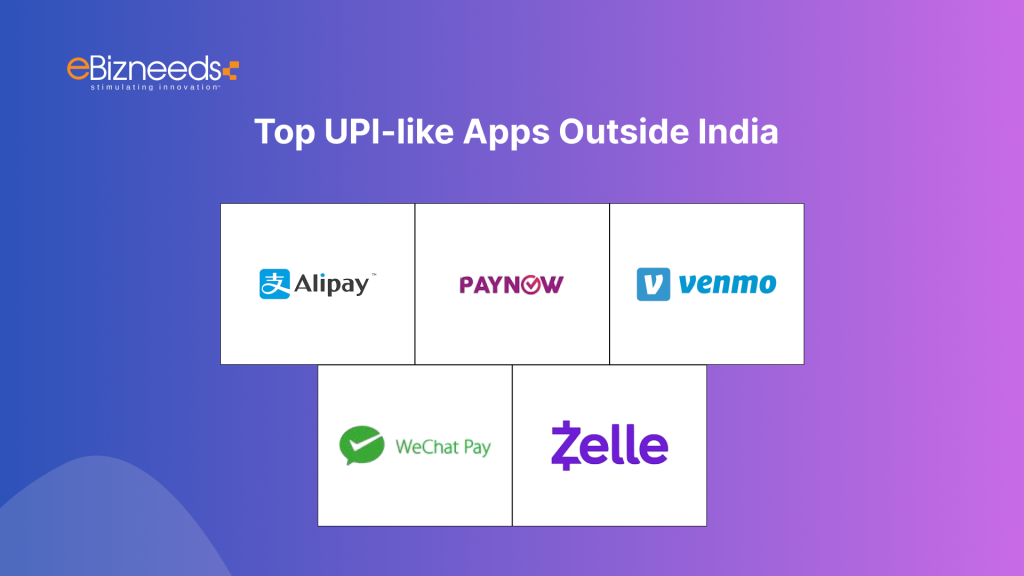

Top UPI-like Apps Outside India

6. Alipay (China)

A global leader in digital payments, offering QR code-based transactions and extensive financial services.

- Key Features: Money transfers, utility payments, and loan services.

- USP: Integration with e-commerce giant Alibaba.

7. PayNow (Singapore)

A fast payment system similar to UPI, enabling instant bank-to-bank transfers using mobile numbers or NRIC.

- Key Features: Cross-border UPI integration and secure real-time payments.

- USP: Collaboration with UPI for cross-border transactions.

8. Venmo (USA)

Popular among millennials, Venmo simplifies peer-to-peer payments and social sharing.

- Key Features: Split payments, social feeds, and payment tracking.

- USP: Social media-style payment sharing.

9. WeChat Pay (China)

A payment feature within WeChat, allowing users to send money and pay merchants.

- Key Features: QR code payments and integration with social media.

- USP: Widespread use due to its integration with the popular messaging app.

10. Zelle (USA)

A UPI-like system allowing instant transfers between US bank accounts.

- Key Features: No app-specific wallet, direct transfers between bank accounts.

- USP: Bank-led payment solution with no additional fees.

These apps highlight the global potential of UPI-like systems in simplifying digital payments.

Whether in India or abroad, the increasing reliance on these platforms underscores the need for businesses to develop UPI apps to stay competitive and meet growing user demands.

Reasons to Develop a UPI App

Developing a fintech app like one we are talking about here is more than just joining the digital payment trend – it’s about tapping into a rapidly growing market with unmatched potential.

Here are the top three reasons why businesses should consider investing in UPI app development:

1. Explosive Growth of Digital Payments

The digital payment market is experiencing exponential growth, and UPI is leading the charge:

- Over 12 billion monthly UPI transactions were recorded in December 2024, reflecting its immense popularity.

- As UPI expands internationally, the potential user base is no longer limited to India, making it a global phenomenon.

By creating a UPI app, you can position your business at the forefront of this booming market.

2. Minimal Transaction Costs for Users and Merchants

One of the biggest advantages of UPI is its affordability:

- Zero Merchant Discount Rate (MDR) encourages small businesses to adopt UPI, expanding the user base rapidly.

- Low or no transaction fees for users make it highly appealing compared to costly alternatives like credit cards or international payment gateways.

This cost-effectiveness allows businesses to attract and retain more users.

3. All-in-One Financial Solution

Unlike traditional payment systems, UPI offers a comprehensive financial ecosystem that includes:

- Money transfers (peer-to-peer and peer-to-merchant).

- Bill payments and subscriptions.

- Loan management and recurring payments.

With such diverse functionality, a UPI app caters to a wide range of customer needs, enhancing user engagement and satisfaction.

Countries like Singapore, UAE, and Bhutan are already integrating UPI into their systems.

This global expansion means developing a UPI app now will position your business to capitalize on cross-border payment opportunities in the near future.

If you’re considering building your own UPI app, the next step is understanding the development process in detail. .

UPI App Development Process: Step-by-Step Guide

Developing a UPI app involves a meticulous process that ensures the app is secure, user-friendly, and compliant with regulatory standards.

Here’s a step-by-step breakdown of how to successfully create a robust UPI app:

Step 1: Research and Planning

Before diving into development, conduct detailed research to:

- Understand user needs: What features and functionalities do your target users want?

- Analyze competitors: Study existing UPI apps like PhonePe, Google Pay, and Paytm to identify gaps in the market.

- Define objectives: Set clear goals for your app, such as transaction volume, user base growth, or revenue targets.

This foundation will guide the entire development process.

Step 2: Partner with Banks and NPCI

Collaborate with banks and obtain necessary approvals to integrate your app into the UPI ecosystem.

- Sponsor Bank: Identify a bank that will act as your payment service provider (PSP).

- NPCI Compliance: Ensure your app meets NPCI’s technical and security requirements for UPI integration.

Step 3: UI/UX Design

Design a user-friendly interface that emphasizes simplicity and accessibility:

- Key considerations: Easy navigation, minimal clicks for transactions, and responsive design for different devices.

- Additional features: Include visual cues for users, such as QR code scanning or transaction history.

A seamless design enhances user retention and satisfaction.

Step 4: Backend Development

The backend is the backbone of your UPI app, responsible for handling transactions and ensuring security:

- APIs Integration: Integrate APIs for UPI payment processing, bank account linking, and fraud detection.

- Security Features: Implement encryption, two-factor authentication, and real-time monitoring to safeguard user data.

- Scalability: Build an architecture that can handle millions of transactions without performance issues.

Step 5: Frontend Development

Develop the app’s frontend to ensure it’s intuitive and visually appealing:

- Use frameworks like React Native or Flutter for cross-platform compatibility.

- Test for responsiveness on different devices, ensuring a consistent experience.

Step 6: Security and Compliance

Compliance is critical when dealing with financial transactions. Ensure your app:

- Adheres to NPCI guidelines for UPI payment systems.

- Implements RBI mandates like data encryption and secure payment gateways.

- Conducts regular security audits to identify and resolve vulnerabilities.

Step 7: Testing

Rigorous testing ensures your app is bug-free and delivers a seamless user experience:

- Functional Testing: Verify that all features work as intended.

- Load Testing: Assess app performance under high transaction volumes.

- Usability Testing: Ensure the app is easy to navigate for all user demographics.

Step 8: Deployment

Launch your UPI app on app stores (Google Play and Apple App Store) with optimized descriptions and marketing campaigns.

Work with your sponsor bank and NPCI to finalize the deployment.

Step 9: Post-Launch Maintenance

Once your app is live, continuous maintenance and support are crucial:

- Address user feedback promptly.

- Update features to stay competitive.

- Ensure compliance with evolving regulatory requirements.

By following these steps, you can develop a secure and user-friendly UPI app that meets industry standards and user expectations.

Cost to Develop a UPI App

The cost to develop a UPI app depends on several factors, including the complexity of features, the app’s design, compliance requirements, and the development team’s expertise.

So, what’s the average cost to develop a UPI app? Well, it looks something like this:

- Basic UPI App: $50,000 – $70,000

- Advanced UPI App: $80,000 – $150,000

Fintech app development cost can be difficult to predict. That’s why, below we will look at a brief overview of the cost components and their impact.

| Cost Factor | Description | Estimated Cost Range (USD) |

| UI/UX Design | Creating user-friendly, visually appealing interfaces. | $5,000 – $15,000 |

| Backend Development | Building a scalable architecture for transaction processing and security. | $20,000 – $50,000 |

| API Integration | Integrating with UPI APIs, bank systems, and third-party services. | $10,000 – $20,000 |

| Compliance and Security | Ensuring adherence to NPCI, RBI, and global data security standards. | $10,000 – $30,000 |

| Testing and Quality Assurance | Conducting functional, load, and security testing. | $5,000 – $10,000 |

| Post-Launch Maintenance | Ongoing updates, feature enhancements, and user support. | $2,000 – $5,000 per month |

| Marketing and Launch | Promoting the app through digital campaigns and app store optimization (ASO). | $5,000 – $10,000 |

This cost estimate may vary based on your app’s complexity, geographical location of your development team, and additional integrations like AI-powered fraud detection or cross-border payment functionality.

Developing a UPI app is a significant investment, but the potential ROI from the rapidly growing digital payment market makes it worth every dollar.

Essential & Advanced Features for a UPI App

To create a successful UPI app, you need to integrate features that offer users convenience, security, and versatility.

Below is a list of essential and advanced features that can make your app stand out in the competitive digital payment market:

Essential Features

- User Registration and Login

- Simple onboarding with mobile number verification and UPI ID creation.

- Bank Account Linking

- Secure linking of multiple bank accounts through UPI.

- Send and Receive Money

- Instant peer-to-peer (P2P) and peer-to-merchant (P2M) transactions.

- QR Code Scanner

- Enable quick payments by scanning merchant or personal QR codes.

- Transaction History

- View detailed logs of completed, pending, and failed transactions.

- Bill Payments

- Pay utility bills like electricity, water, gas, and mobile recharges directly from the app.

- Real-Time Notifications

- Send alerts for successful payments, failed transactions, and offers.

- UPI PIN Management

- Securely create, update, or reset the UPI PIN for linked accounts.

- Customer Support

- Integrated chatbots or helplines to resolve user issues promptly.

Advanced Features

- Multi-Language Support

- Include regional and international languages for a broader audience reach.

- Recurring Payments (UPI AutoPay)

- Set up automated payments for subscriptions or loans.

- AI-Powered Fraud Detection

- Use machine learning algorithms to detect suspicious activity and prevent fraud.

- Cross-Border Payments

- Enable international money transfers using UPI-compatible systems like PayNow.

- Personalized Offers and Rewards

- Provide cashback, discounts, or referral bonuses to boost user engagement.

- Voice-Assisted Transactions

- Integrate voice commands for hands-free payments.

- Expense Tracking and Analytics

- Offer insights into spending patterns and budgeting tools.

- Integration with Wearables

- Allow transactions through smartwatches and other wearable devices.

- Merchant Dashboard

- Provide merchants with tools to track payments, generate invoices, and manage sales.

- Biometric Authentication

- Use fingerprint or facial recognition for enhanced security.

The combination of essential and advanced features ensures your app caters to a wide range of user needs.

By including innovative functionalities like AI fraud detection and cross-border payments, you can attract more users and set your app apart from competitors.

Monetization Strategies for a UPI App

Building a UPI app not only enhances user experiences but also offers multiple opportunities to generate revenue.

Here are the most effective monetization methods tailored to the industry, along with their potential benefits:

1. Transaction Fees for Value-Added Services

While UPI transactions are generally free, you can charge users for premium or value-added services such as:

- International Transactions: Apply a small fee for cross-border payments.

- Priority Processing: Offer faster settlements for high-value transactions.

Potential: These fees can significantly boost your revenue, especially if your app targets businesses or premium users.

2. Subscription Plans

Introduce subscription models for additional features such as:

- Expense management tools.

- Advanced analytics for users and merchants.

- Ad-free experiences.

Potential: Subscription-based models provide recurring income, making your app financially sustainable.

3. Merchant Solutions

Charge merchants for:

- Access to detailed sales analytics and dashboards.

- Premium listing or promotional features within your app.

- UPI AutoPay setup for recurring payments.

Potential: Given the growing merchant adoption of UPI, these solutions can be a significant revenue stream.

4. Advertisements and Promotions

Allow brands or merchants to promote their products/services within your app:

- Display ads for specific products or services.

- Sponsored listings or banners for merchants.

Potential: Ad placements can generate substantial revenue, especially if your app has a large user base.

5. Partner Commissions

Collaborate with third-party services like insurance providers, loan providers, or investment platforms to:

- Offer their services through your app.

- Earn a commission on each successful transaction.

Potential: Financial partnerships can drive both user engagement and revenue.

6. Data Insights as a Service

Aggregate anonymized data to provide valuable market insights to businesses and financial institutions, such as:

- Spending patterns.

- Consumer preferences.

Potential: Selling anonymized data insights can be a lucrative opportunity, provided it complies with data privacy regulations.

7. Cross-Promotional Strategies

Partner with e-commerce platforms or service providers to:

- Offer exclusive discounts or cashback deals.

- Take a share of the revenue from sales driven through your app.

Potential: This method boosts both user engagement and app profitability.

A well-thought-out monetization strategy ensures that your UPI app remains financially viable while delivering value to users and merchants.

By combining these methods, you can achieve sustainable revenue growth while maintaining user satisfaction.

Technology Trends Shaping UPI App Development

Here’s a table summarizing the key technology trends that are influencing UPI app development, their features, and their potential impact:

| Technology Trend | Description | Impact on UPI Apps |

| AI and Machine Learning | Real-time analysis of user behavior to detect and prevent fraudulent activity. | Enhanced security and user trust by reducing fraud rates. |

| Blockchain for Payments | Ensures transparent, secure, and fast international money transfers. | Reduced cross-border transaction costs and eliminated intermediaries. |

| Voice-Activated Payments | Enables hands-free transactions using voice recognition. | Simplifies the user experience, improving accessibility for all users. |

| Biometric Authentication | Uses fingerprint and facial recognition for secure logins and payments. | Offers seamless security, enhancing user confidence and convenience. |

| IoT Integration | Connects UPI apps to devices like smartwatches and smart speakers. | Facilitates easy payments via wearables and IoT devices, improving access. |

| Big Data Analytics | Analyzes user behavior to deliver personalized offers and insights. | Boosts user engagement and retention through tailored experiences. |

| Cloud-Based Infrastructure | Stores data and manages heavy loads using cloud technology. | Ensures scalability and reliability during peak transaction periods. |

| Enhanced QR Code Technology | Uses dynamic QR codes with advanced encryption for secure payments. | Improves payment speed and security while reducing fraud risks. |

| 5G and Edge Computing | Provides faster connections and reduces latency for real-time transactions. | Enables smoother high-volume transactions for users and merchants. |

Incorporating these technology trends into your UPI app development ensures your app stays ahead of the curve.

These advancements not only enhance functionality and security but also improve user satisfaction and scalability.

Challenges in UPI App Development and How to Overcome Them

Developing a UPI app comes with its own set of challenges, ranging from technical complexities to regulatory compliance.

However, with the right strategies, these hurdles can be effectively managed.

Below is a detailed table outlining the key challenges and their solutions:

| Challenge | Description | Solution |

| Regulatory Compliance | Ensuring the app meets stringent NPCI and RBI guidelines for UPI integration. | Partner with experts in fintech compliance and regularly update the app to adhere to regulations. |

| Security Concerns | Protecting user data and transactions from fraud and cyberattacks. | Implement encryption, two-factor authentication, real-time fraud detection, and biometric logins. |

| Scalability Issues | Handling millions of transactions during peak periods without app crashes. | Use cloud-based infrastructure and microservices architecture for seamless scalability. |

| Integration with Banks | Establishing partnerships and technical integration with sponsor banks. | Collaborate with reliable banks early in the development process and ensure proper API testing. |

| User Trust and Adoption | Convincing users to trust a new app for financial transactions. | Focus on user education, provide a demo, and highlight security features in your marketing. |

| Cross-Border Compatibility | Adapting the app for international payments in compliance with global standards. | Integrate blockchain and partner with international payment networks for smoother transactions. |

| High Development Costs | The cost of building a feature-rich UPI app can be significant. | Prioritize essential features during the MVP stage and scale gradually based on user feedback. |

| Technical Downtime | Ensuring app reliability during server maintenance or unforeseen issues. | Use load balancers and maintain a robust disaster recovery plan to minimize downtime. |

| Competition in the Market | Standing out in a crowded space with well-established players. | Focus on unique features, personalization, and superior user experience to differentiate your app. |

Overcoming these challenges ensures the development of a secure, reliable, and user-friendly UPI app.

By addressing these pain points early in the development process, you can build an app that not only complies with regulations but also wins user trust and loyalty.

eBizneeds – Your Trusted Partner for UPI App Development

Building a UPI app requires expertise, precision, and a deep understanding of the fintech landscape.

At eBizneeds, we specialize in creating secure, scalable, and feature-rich UPI applications tailored to meet your business needs.

- Expertise in Fintech Solutions: With years of experience in developing fintech apps, we understand the technical and regulatory requirements of UPI systems.

- Customized Development: We design apps that align with your business goals, ensuring they are user-friendly, secure, and compliant with NPCI and RBI standards.

- Cutting-Edge Technology: From AI-powered fraud detection to blockchain integration, we leverage the latest technologies to make your app future-ready.

- End-to-End Support: From planning to post-launch maintenance, our team provides 360° support to ensure your app’s success.

- Cost-Effective Solutions: Our development process focuses on delivering high-quality apps without exceeding your budget.

Partner with eBizneeds, a leading fintech app development company, to turn your app idea into a reality. Whether you’re targeting local or global markets, our team will help you create an app that stands out.

Conclusion

Developing a UPI app is an excellent opportunity to tap into the ever-growing digital payment market. With a well-defined process, innovative features, and a robust monetization strategy, your app can cater to millions of users and drive significant revenue. By addressing challenges and embracing the latest technology trends, you can create a seamless payment experience for your users.

FAQs

The cost typically ranges from $50,000 to $150,000, depending on features, complexity, and compliance requirements

It takes around 4 to 8 months, depending on the app’s scope and functionality.

A robust UPI app should include two-factor authentication, encryption, real-time fraud detection, and biometric authentication

Yes, UPI apps can support cross-border transactions by integrating with compatible systems like PayNow or blockchain networks.

eBizneeds offers customized solutions, cutting-edge technologies, and end-to-end support, ensuring your UPI app is secure, scalable, and market-ready.

Naveen Khanna is the CEO of eBizneeds, a company renowned for its bespoke web and mobile app development. By delivering high-end modern solutions all over the globe, Naveen takes pleasure in sharing his rich experiences and views on emerging technological trends. He has worked in many domains, from education, entertainment, banking, manufacturing, healthcare, and real estate, sharing rich experience in delivering innovative solutions.