Have you ever thought about how digital payments have revolutionized the way we handle money? From paying bills to splitting dinner expenses, eWallets have become a modern necessity.

Starting an eWallet business isn’t just about jumping on the trend-it’s about tapping into a market that’s growing faster than ever. With the rise in smartphone usage and demand for seamless transactions, eWallets are no longer a luxury but a part of everyday life.

In this blog, we’ll walk you through everything you need to know about launching your own eWallet business-from understanding its foundation to ensuring a successful launch. Whether you’re looking to cater to tech-savvy millennials or businesses that rely on secure payment solutions, this guide has you covered.

So, are you ready to take your first step toward creating a game-changing eWallet platform? Let’s dive in!

What is an eWallet Business?

An eWallet business revolves around providing digital payment solutions that allow users to store, send, and receive money electronically. Think of it as a virtual wallet that resides on your smartphone, offering the convenience of managing your finances without carrying physical cash or cards.

From peer-to-peer (P2P) transfers to paying for groceries or streaming services, eWallets have become the backbone of modern financial transactions. These platforms often include features like secure payment gateways, loyalty rewards, and integrations with various services to enhance user experience.

But what makes an eWallet business stand out? It’s the ability to address diverse user needs, from individual users seeking simplicity to businesses requiring advanced payment processing systems.

In short, an eWallet business offers:

- Convenience: Easy money transfers with just a few clicks.

- Security: Advanced encryption and fraud detection.

- Flexibility: Payments for a variety of goods, services, and utilities.

By understanding the essence of eWallets, you can shape your business idea to cater to specific target audiences, whether it’s consumers or enterprises.

Ready to explore the different types of eWallet businesses you can build? Let’s move forward!

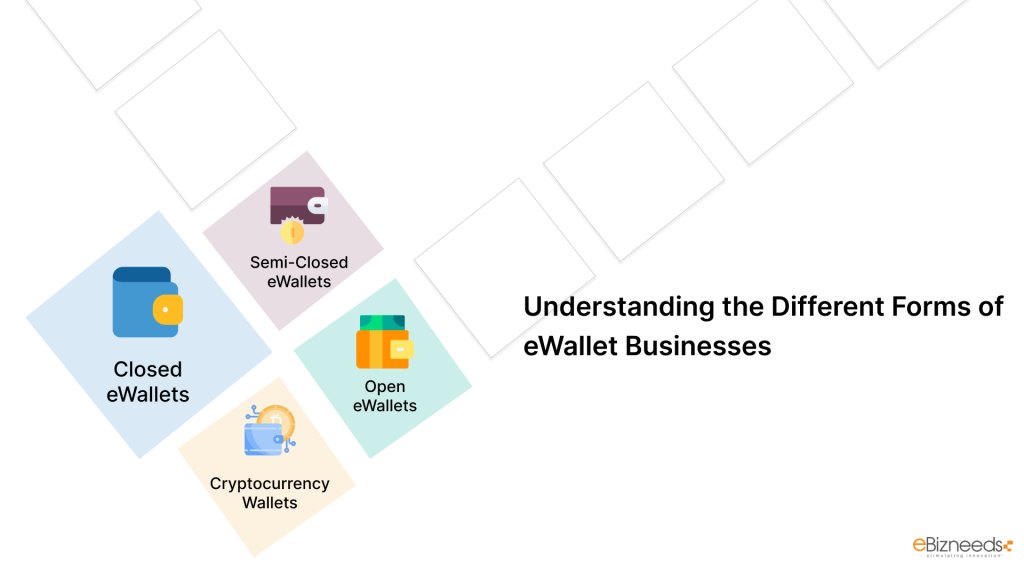

Understanding the Different Forms of eWallet Businesses

Not all eWallets are the same-they cater to various needs, markets, and user preferences. To succeed, you need to understand the key types of eWallet businesses and decide which aligns best with your goals.

1. Closed eWallets

A closed eWallet is specific to a particular company or ecosystem. Users can only spend the funds within that company’s services or products. Think of online retail giants like Amazon or ride-hailing services like Uber.

Example: Amazon Pay

Best For: Businesses offering their own services/products.

2. Semi-Closed eWallets

These eWallets are more flexible, allowing users to transact with multiple merchants, provided the merchants have signed an agreement with the eWallet provider. It’s a popular choice for businesses that want to expand their reach.

Example: Paytm, Venmo

Best For: Companies wanting to collaborate with various retailers and service providers.

3. Open eWallets

Open eWallets offer complete freedom, allowing users to send and receive money, withdraw cash at ATMs, and make purchases anywhere. They require partnerships with banks and other financial institutions.

Example: PayPal, Google Pay

Best For: Businesses aiming to dominate the digital payment ecosystem.

4. Cryptocurrency Wallets

These wallets cater to the growing demand for digital currencies like Bitcoin and Ethereum. They store cryptocurrencies securely and facilitate seamless transactions.

Example: Coinbase Wallet, Trust Wallet

Best For: Tech-savvy businesses catering to crypto enthusiasts.

Understanding these forms will help you define your business model, target audience, and technology needs. Each type has its pros and cons, so choose one that aligns with your vision.

Let’s move to why starting an eWallet business could be the game-changer you’re looking for!

Why Should You Start an eWallet Business?

The eWallet industry is booming, and for good reasons.

It’s not just a trend but a pivotal shift in how people manage their finances. Starting an eWallet business offers a golden opportunity to tap into a fast-growing market, and here’s why:

1. Massive Market Growth

The global digital payments market is expected to grow at an astounding pace, driven by increased smartphone usage, internet penetration, and demand for contactless payment solutions.

This means more customers are moving away from traditional cash transactions and embracing digital wallets.

Why it matters to you:

The market’s upward trajectory ensures a steady demand for your eWallet services.

2. Shifting Consumer Preferences

Consumers value convenience and speed. eWallets eliminate the need to carry cash, handle cards, or even visit a physical bank.

They also provide features like instant payments, transaction histories, and loyalty rewards, making them irresistible.

Why it matters to you:

Meeting consumer demand means higher adoption rates and user satisfaction.

3. Support for Small Businesses

eWallets aren’t just for individual users. Small businesses are increasingly adopting them to streamline transactions and reduce dependency on cash.

By integrating with businesses, you can offer them payment processing solutions that simplify their operations.

Why it matters to you:

It opens up additional revenue streams by targeting B2B clients.

4. Government Push for Cashless Economies

Governments worldwide are promoting cashless transactions to reduce corruption, enhance transparency, and improve efficiency.

This creates a supportive environment for launching and growing an eWallet platform.

Why it matters to you:

Government incentives and policies can reduce entry barriers and help scale your business.

5. Recurring Revenue Opportunities

eWallets provide multiple ways to generate ongoing revenue, from transaction fees to subscription plans for premium users.

Why it matters to you:

A diversified revenue model ensures consistent cash flow.

6. Untapped Potential in Niche Markets

While giants like PayPal dominate, there’s still room for niche players who can offer specialized solutions, such as regional payment systems or sector-specific wallets (e.g., healthcare or education).

Why it matters to you:

Carving out a niche can help you stand out in a competitive market.

By starting an eWallet business, you’re not just building a service; you’re creating a solution for modern financial challenges. With the right strategy, the potential for success is limitless.

Ready to take the first step? Let’s explore how you can prepare to launch your eWallet business effectively!

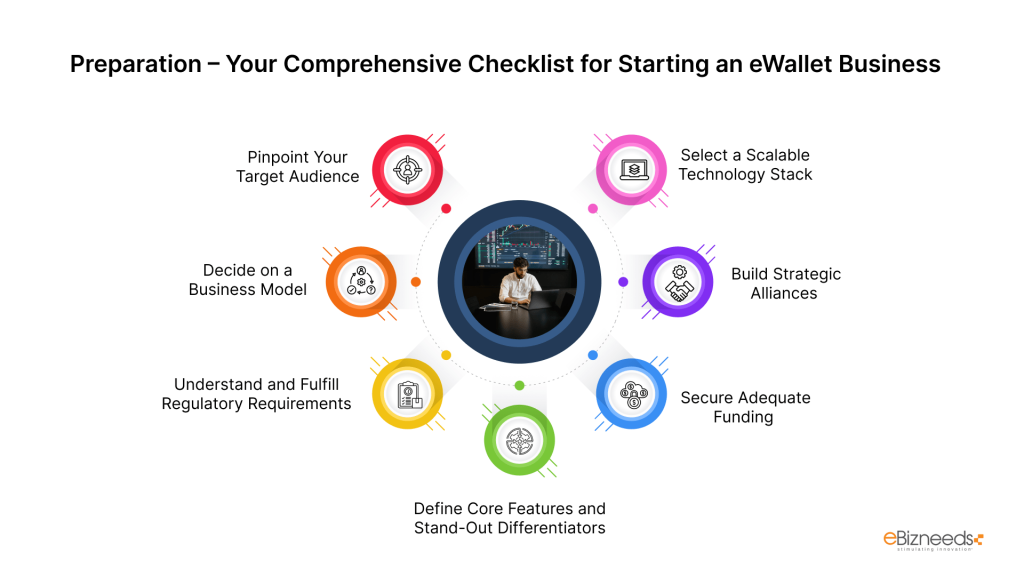

Step 1: Preparation – Your Comprehensive Checklist for Starting an eWallet Business

Building an eWallet business starts with a thorough preparation phase. This step is all about understanding the intricacies of your market, creating a robust framework, and aligning your resources with your goals. Let’s break down this preparation process in detail:

1. Pinpoint Your Target Audience

Defining your audience is a critical first step. A clear understanding of your users ensures that your platform meets their specific needs.

Questions to Consider:

- Are you targeting individual users, small businesses, or enterprise clients?

- What pain points will your platform solve?

- Are your users in urban areas, rural regions, or spread across the globe?

Example:

- If your audience includes businesses, focus on features like invoice generation and payroll processing.

- For tech-savvy consumers, include digital card management and QR code payments.

Actionable Tip: Conduct market research, focus groups, and surveys to identify unmet needs and tailor your platform accordingly.

2. Decide on a Business Model

Your business model determines the scope and usability of your eWallet. Each model offers unique advantages:

- Closed Wallet: Exclusively for your ecosystem (e.g., for retail or service-based companies).

- Semi-Closed Wallet: Usable at partnered merchants, offering flexibility for users.

- Open Wallet: Enables full financial services, including ATM withdrawals and international transactions.

- Cryptocurrency Wallet: Targets the growing crypto community, enabling secure storage and transactions.

Example:

If you aim to support small businesses, a semi-closed wallet integrated with local merchants may be the best fit.

Actionable Tip: Choose a model that aligns with your budget, resources, and long-term vision.

3. Understand and Fulfill Regulatory Requirements

Navigating the regulatory landscape is crucial. Laws governing digital payments vary by country, and non-compliance can lead to hefty penalties.

Steps to Take:

- Research licensing requirements in your target markets (e.g., Payment Service Provider licenses).

- Ensure compliance with data protection regulations like GDPR (Europe), CCPA (California), or HIPAA (for healthcare).

- Implement secure KYC (Know Your Customer) processes to verify users.

Actionable Tip: Consult legal experts specializing in fintech to streamline compliance and avoid legal pitfalls.

4. Define Core Features and Stand-Out Differentiators

Your eWallet platform’s success hinges on its ability to offer value-added services. List the essential features first, then identify what will make your platform unique.

Essential Features:

- Easy onboarding and account setup.

- Peer-to-peer payments.

- Multi-currency support.

- Robust security protocols like two-factor authentication.

Unique Selling Points (USPs):

- Advanced AI fraud detection.

- Personalized spending analytics.

- Blockchain for transparent and secure transactions.

Actionable Tip: Conduct competitor analysis to find gaps in their offerings and build those as your USPs.

5. Secure Adequate Funding

Developing an eWallet platform is resource-intensive. You’ll need funds for software development, marketing, legal compliance, and customer support.

Funding Sources:

- Venture capital or angel investors.

- Government grants for fintech innovation.

- Partnerships with banks or financial institutions.

Breakdown of Costs:

- Development: $50,000–$150,000 (depending on complexity).

- Licensing & Legal: $10,000–$30,000.

- Marketing: $5,000–$20,000 per campaign.

Actionable Tip: Prepare a professional business plan with financial projections to attract investors.

6. Build Strategic Alliances

Partnerships are the backbone of an eWallet’s functionality and credibility.

Partnership Opportunities:

- Collaborate with banks or payment gateways for seamless transactions.

- Partner with merchants to expand usability.

- Work with technology providers for cloud storage and cybersecurity solutions.

Example: PayPal’s partnerships with e-commerce platforms like Shopify expanded its reach and usability.

Actionable Tip: Start small with a few key partnerships, then scale as your business grows.

7. Select a Scalable Technology Stack

Choosing the right technology ensures a smooth user experience and prepares your platform for future growth.

Tech Requirements:

- A secure payment gateway for transactions.

- Cloud-based architecture for scalability.

- Mobile app frameworks for Android and iOS.

- Advanced encryption standards to safeguard data.

Actionable Tip: Engage experienced developers or partner with an eWallet app development company like eBizneeds to ensure a reliable and efficient platform.

With thorough preparation, you’ll lay the groundwork for a successful eWallet business. Ready to take the next step? Let’s delve into the product development phase and bring your vision to life!

Step 2: Product Development – Building Your eWallet Platform

Once your preparation is complete, it’s time to bring your eWallet vision to life. The product development phase involves creating a user-friendly, secure, and feature-rich platform that sets you apart from competitors. Here’s how to do it step by step:

1. Define Your Platform’s Architecture

The architecture is the backbone of your eWallet platform. A well-structured system ensures seamless operations and scalability.

Key Components:

- Frontend: User interface for mobile apps and web portals.

- Backend: Server-side logic for transactions, authentication, and integrations.

- Database: Secure storage for user data and transaction records.

- API Layer: Connects your platform with banks, payment gateways, and third-party services.

Example: Use microservices architecture to allow independent updates to different features like payments, notifications, or analytics.

Actionable Tip: Plan your architecture with scalability in mind to accommodate future growth.

2. Design a User-Friendly Interface (UI/UX)

Your platform’s success depends heavily on how easy and enjoyable it is to use.

UI/UX Best Practices:

- Simplify onboarding with quick sign-up options.

- Use clear labels and instructions for transactions.

- Provide real-time feedback for actions (e.g., “Payment Successful” notifications).

- Optimize for both mobile and web users.

Actionable Tip: Conduct usability testing with real users to identify and fix pain points before launch.

3. Develop Essential Features

Your eWallet must offer features that cater to your target audience while ensuring security and ease of use.

Core Features to Include:

- User Registration: Secure sign-up using email, phone numbers, or social media accounts.

- KYC Integration: Identity verification to comply with regulations.

- Transaction Management: Peer-to-peer payments, bill payments, and QR code scanning.

- Security Features: Multi-factor authentication, data encryption, and fraud detection.

- Push Notifications: Alerts for transactions, offers, and updates.

Actionable Tip: Prioritize features based on user needs and release advanced functionalities in future updates.

4. Integrate with Third-Party Services

To ensure smooth transactions and expand functionality, integrate your platform with reliable third-party providers.

Essential Integrations:

- Payment Gateways: Stripe, PayPal, or Razorpay.

- Banks and Financial Institutions: For secure fund transfers.

- Third-Party APIs: For services like currency conversion or real-time analytics.

Actionable Tip: Vet third-party providers carefully to ensure they align with your platform’s security and performance standards.

5. Ensure Robust Security

Security is non-negotiable in the eWallet industry. Users must trust your platform to handle their sensitive financial data.

Security Measures:

- Data encryption using protocols like AES-256.

- Tokenization for sensitive information like credit card numbers.

- Regular penetration testing to identify vulnerabilities.

Actionable Tip: Stay updated on cybersecurity trends and proactively upgrade your security measures.

6. Choose the Right Development Approach

Decide whether to build your platform in-house or outsource development.

Options:

- In-House Team: Full control over development but requires significant resources.

- Outsourcing: Partner with an experienced eWallet app development company like eBizneeds for a cost-effective, professional solution.

Actionable Tip: If outsourcing, look for a team with proven expertise in fintech and a strong portfolio of similar projects.

7. Test Extensively Before Launch

Testing is a critical step to ensure your platform is bug-free, secure, and user-ready.

Testing Phases:

- Functional Testing: Verify that all features work as intended.

- Security Testing: Assess vulnerability to hacking and fraud.

- Usability Testing: Gather feedback from real users on ease of use.

Actionable Tip: Use automated testing tools alongside manual testing for comprehensive coverage.

8. Set Up a Maintenance Plan

Your eWallet platform requires ongoing maintenance to ensure smooth performance and handle updates.

Maintenance Tasks:

- Monitor servers and database performance.

- Roll out updates for new features and security enhancements.

- Provide 24/7 customer support to address user issues.

Actionable Tip: Allocate a dedicated budget and team for maintenance from the start.

By focusing on these detailed steps, you’ll create a robust and feature-rich eWallet platform that resonates with users. Next, let’s explore how to successfully launch your eWallet business and captivate your audience!

Step 3: Launching Your eWallet Business – The Roadmap to Success

After thorough preparation and development, it’s time to launch your eWallet business. A strategic launch ensures your platform gains visibility, builds trust, and attracts early users. Here’s a step-by-step guide for a successful launch:

1. Conduct a Soft Launch

Before a full-scale launch, test your platform in a controlled environment. This allows you to gather feedback, identify issues, and make necessary adjustments.

Steps for a Soft Launch:

- Release the platform to a limited audience, such as a specific region or group of beta users.

- Monitor user interactions and system performance.

- Gather feedback on features, usability, and overall experience.

Actionable Tip: Use analytics tools to track key metrics like user retention, transaction success rates, and error reports.

2. Create a Marketing Plan

Your marketing strategy will determine how quickly your eWallet gains traction. Focus on building excitement and trust around your product.

Key Marketing Tactics:

- Social Media Campaigns: Share teasers, tutorials, and user testimonials on platforms like Instagram, Facebook, and LinkedIn.

- Influencer Partnerships: Collaborate with fintech influencers or business leaders to endorse your eWallet.

- Email Marketing: Reach potential users with personalized emails explaining your platform’s benefits.

- Content Marketing: Publish blogs, videos, and infographics highlighting features and use cases.

Actionable Tip: Launch a referral program to incentivize existing users to bring in new ones.

3. Offer Launch Incentives

Attract early adopters by offering rewards that encourage them to try your eWallet.

Examples of Incentives:

- Cashback on first transactions.

- Discounts for partnered merchants.

- Loyalty points for referrals and frequent usage.

Actionable Tip: Highlight these offers in your marketing campaigns to maximize reach.

4. Ensure Strong Customer Support

Excellent customer support builds trust and reduces churn. Users should have an easy way to resolve issues or ask questions.

Customer Support Essentials:

- Provide 24/7 support via chat, email, or phone.

- Create a detailed FAQ section on your website or app.

- Offer multilingual support if targeting international users.

Actionable Tip: Use AI chatbots to handle common queries efficiently, saving resources for complex issues.

5. Leverage PR and Media Coverage

Get your eWallet platform featured in industry blogs, news outlets, and fintech forums to boost credibility and awareness.

Steps to Secure Media Coverage:

- Write and distribute press releases announcing your launch.

- Highlight your platform’s unique features and benefits.

- Reach out to journalists and bloggers in the fintech space.

Actionable Tip: Share success stories or testimonials from your soft launch to strengthen your pitch.

6. Monitor Performance Metrics Post-Launch

Once your eWallet is live, tracking its performance is crucial for making data-driven improvements.

Metrics to Track:

- Daily Active Users (DAU) and Monthly Active Users (MAU).

- Average Transaction Value (ATV).

- User Retention and Churn Rates.

- Customer Satisfaction Scores (CSAT).

Actionable Tip: Use feedback surveys and app store reviews to understand user preferences and concerns.

7. Scale Gradually

Avoid rushing into expansions. Instead, grow your eWallet business step by step, ensuring the platform can handle increased demand.

Scaling Strategies:

- Introduce new features based on user requests (e.g., bill payments, international transfers).

- Expand your partnerships with banks, merchants, and service providers.

- Enter new geographic markets with localized versions of your platform.

Actionable Tip: Invest in server capacity and cybersecurity to support scaling without compromising performance.

Launching your eWallet business is a critical milestone. By planning each step carefully and focusing on user satisfaction, you set the stage for long-term success. Up next, we’ll explore the challenges you might face and how to overcome them effectively.

Challenges You Might Face & Their Solutions

Starting and running an eWallet business is an exciting venture, but it’s not without challenges. Identifying potential roadblocks and preparing solutions in advance will help you navigate the journey smoothly. Let’s explore the most common challenges and how to tackle them:

1. Regulatory Compliance

Digital payment platforms operate in a highly regulated environment. Failing to meet these requirements can result in legal actions or fines.

Challenges:

- Navigating complex regulations that vary across regions.

- Acquiring licenses for operating financial services.

- Complying with anti-money laundering (AML) and Know Your Customer (KYC) laws.

Solutions:

- Hire a legal consultant specializing in fintech to ensure compliance.

- Use APIs for seamless KYC integration to automate verification.

- Stay updated on regional regulatory changes and adapt accordingly.

Example: Paytm expanded successfully by aligning with India’s payment regulatory framework.

2. Ensuring Platform Security

Security concerns are among the biggest barriers to user adoption. Breaches can lead to financial loss and damage your platform’s reputation.

Challenges:

- Preventing data breaches and cyberattacks.

- Securing user data from unauthorized access.

- Complying with data protection laws like GDPR or CCPA.

Solutions:

- Implement multi-factor authentication (MFA) for account access.

- Use encryption protocols like AES-256 for data security.

- Conduct regular security audits and penetration testing.

3. Building User Trust

Users are often hesitant to trust new platforms with their financial data, especially in a competitive market.

Challenges:

- Overcoming skepticism about safety and reliability.

- Competing against established players with strong brand recognition.

Solutions:

- Highlight your security features and compliance certifications in your marketing.

- Showcase testimonials and case studies from early adopters.

- Provide responsive and empathetic customer support to address user concerns.

4. Achieving Scalability

As your eWallet gains users, scaling the platform to handle increased demand is essential.

Challenges:

- Managing server downtime or slow processing during peak times.

- Adding new features without disrupting existing functionalities.

Solutions:

- Opt for cloud-based infrastructure to ensure scalability.

- Use load balancers to distribute traffic evenly across servers.

- Implement microservices architecture to make updates seamless.

Example: Google Pay’s smooth scalability has allowed it to serve millions of users without compromising speed.

5. Maintaining Competitive Edge

The eWallet industry is highly competitive, with giants like PayPal and Google Pay dominating the market.

Challenges:

- Standing out amidst well-established competitors.

- Keeping up with emerging trends and user expectations.

Solutions:

- Focus on niche markets (e.g., regional users, specific industries).

- Introduce unique features like AI-powered spending insights or cryptocurrency support.

- Regularly update your app with enhancements based on user feedback.

6. High Initial Development and Marketing Costs

Developing and launching an eWallet requires significant financial investment.

Challenges:

- Balancing development costs with limited initial revenue.

- Allocating funds for marketing and user acquisition.

Solutions:

- Start with an MVP (Minimum Viable Product) to reduce upfront costs.

- Seek venture capital funding or government grants for fintech innovations.

- Use cost-effective marketing strategies like referral programs and social media.

7. User Retention

Attracting users is just the beginning-keeping them engaged is the real challenge.

Challenges:

- Users abandoning the platform after initial use.

- Limited usage frequency due to lack of engagement.

Solutions:

- Introduce gamification elements like rewards and streaks for regular usage.

- Provide exclusive offers and discounts for loyal users.

- Use push notifications to remind users about transactions, rewards, and new features.

Challenges are inevitable, but with a proactive approach, each obstacle becomes an opportunity to refine your platform and strengthen your business. In the next section, we’ll look at some of the most successful eWallet businesses and what you can learn from their journeys.

Popular eWallet Businesses & Their Success Stories

Learning from the successes of established eWallet platforms can provide valuable insights for building and scaling your own business.

Let’s dive into some of the most successful eWallet businesses and what makes them stand out.

1. PayPal – The Pioneer of Digital Wallets

Founded: 1998

Market Reach: Operates in over 200 countries.

Success Story:

PayPal revolutionized online transactions by offering secure payments for e-commerce platforms. Its partnership with eBay catapulted its growth, making it synonymous with online payments.

Key Strategies:

- Built trust by prioritizing security with buyer protection policies.

- Expanded services by integrating with financial institutions and e-commerce sites.

- Innovated continuously with features like “Pay in 4” (buy now, pay later).

Lesson: Early adoption of emerging technologies and partnerships with key players can drive exponential growth.

2. Google Pay – Leveraging the Ecosystem

Founded: 2011 (as Google Wallet, rebranded in 2018).

Market Reach: Over 100 million users globally.

Success Story:

Google Pay utilized the massive user base of the Android ecosystem. Seamless integration with Google services made it a go-to option for digital payments.

Key Strategies:

- Simplified payments through one-click functionality.

- Offered loyalty rewards and cashbacks to attract users.

- Tapped into global markets with localized features like UPI in India.

Lesson: Leveraging existing ecosystems and tailoring features for local markets ensures rapid adoption.

Founded: 2009

Market Reach: Primarily in the United States.

Success Story:

Venmo reimagined peer-to-peer payments by adding a social element. Its feed-based interface allowed users to share their transactions, creating a sense of community.

Key Strategies:

- Targeted millennials and Gen Z with a fun, engaging user experience.

- Focused on social sharing and ease of use.

- Monetized through transaction fees for business payments and instant transfers.

Lesson: Adding unique elements like social features can differentiate your platform in a crowded market.

4. Alipay – Dominating the Chinese Market

Founded: 2004

Market Reach: Over 1 billion users.

Success Story:

Alipay became a one-stop shop for payments in China by integrating with e-commerce platforms, utility services, and even public transport systems.

Key Strategies:

- Focused on becoming a “super app” by offering multiple services beyond payments.

- Used QR codes to simplify transactions in a predominantly mobile-first market.

- Partnered with businesses to offer exclusive deals and discounts.

Lesson: Diversification of services can help an eWallet become indispensable to users.

5. Cash App – Simplifying Personal Finance

Founded: 2013

Market Reach: Primarily in the United States and the UK.

Success Story:

Cash App went beyond payments to offer personal finance solutions, such as investing in stocks and cryptocurrency, alongside traditional transactions.

Key Strategies:

- Introduced innovative features like Bitcoin trading.

- Simplified personal finance with savings tools and direct deposits.

- Focused on a user-friendly interface for quick adoption.

Lesson: Expanding into complementary services can create new revenue streams and enhance user retention.

By studying these successful platforms, you can craft a strategy tailored to your target audience and goals. Next, let’s break down the cost of building your eWallet business.

How Much Does It Cost to Start an eWallet Business?

The cost of starting an eWallet business varies depending on factors like platform complexity, features, technology stack, and region.

To help you plan effectively, here’s a detailed breakdown of the key cost components:

1. Development Costs

Developing the eWallet platform is the most significant expense. It includes frontend, backend, and API integration. Here’s breakdown eWallet app development cost:

Breakdown:

- Frontend Development (User Interface): $10,000–$30,000

- Backend Development (Server-side Logic): $20,000–$50,000

- API Integration (Payment Gateways, KYC, etc.): $5,000–$20,000

Factors Affecting Cost:

- Number of features (e.g., multi-currency support, transaction history).

- Type of technology (native apps for iOS/Android vs. hybrid).

- Team size and expertise.

Cost-Saving Tip: Start with an MVP (Minimum Viable Product) to focus on core functionalities first.

2. Licensing and Compliance

Every region has specific licensing requirements for financial services. Non-compliance can result in penalties or bans.

Costs:

- Payment Gateway License: $5,000–$15,000

- KYC/AML Compliance Systems: $10,000–$25,000

- Data Privacy Compliance (e.g., GDPR, CCPA): $2,000–$10,000

Tip: Consult a legal expert to streamline the process and avoid unexpected costs.

3. Security and Encryption

Ensuring robust security is essential for building trust with users.

Security Features:

- Data Encryption: $5,000–$15,000

- Multi-Factor Authentication: $2,000–$7,000

- Fraud Detection Systems: $10,000–$30,000

Cost-Saving Tip: Partner with cybersecurity firms offering affordable packages tailored to fintech startups.

4. Infrastructure and Hosting

Your platform needs a reliable infrastructure to handle user traffic and transactions efficiently.

Breakdown:

- Cloud Hosting (AWS, Google Cloud): $500–$2,000/month

- Server Maintenance: $1,000–$3,000/month

- Scalability Features: $5,000–$10,000

Cost-Saving Tip: Use cloud-based solutions for scalability and lower upfront costs.

5. Design and User Experience

An intuitive and attractive design enhances user satisfaction and retention.

Costs:

- UI/UX Design: $5,000–$15,000

- Usability Testing: $2,000–$5,000

Tip: Prioritize user-friendly navigation and seamless onboarding processes to improve first impressions.

6. Marketing and User Acquisition

Promoting your eWallet to attract users requires a well-planned marketing strategy.

Breakdown:

- Digital Marketing Campaigns: $5,000–$20,000

- Social Media Ads: $2,000–$10,000/month

- Referral Programs and Incentives: $3,000–$10,000

Cost-Saving Tip: Leverage organic marketing tactics like content creation and social media engagement.

7. Maintenance and Updates

After launch, ongoing maintenance ensures your platform remains functional and up-to-date.

Recurring Costs:

- Bug Fixes and Updates: $1,000–$5,000/month

- Customer Support: $2,000–$8,000/month

Tip: Allocate 20–30% of your development budget annually for maintenance and scaling.

| Small-Scale eWallet | $50,000–$100,000 | For regional use with basic features. |

| Mid-Scale eWallet | $100,000–$250,000 | With features like multi-currency support and advanced integrations. |

| Enterprise-Scale eWallet | $250,000–$500,000+ | Comprehensive platform with global reach, high-end security, and advanced features. |

The cost of starting an eWallet business depends on your vision and scale. Starting small and scaling up as demand grows is often the most cost-effective approach. In the next section, we’ll explore how to drive revenue and monetize your eWallet platform effectively.

Driving Revenue Through Your eWallet Business: Monetization Methods

Once your eWallet platform is live, the next step is to ensure it generates consistent revenue.

Monetizing an eWallet effectively requires understanding your users’ needs and aligning them with strategies that create value while maximizing your profits.

Here are proven methods to drive revenue:

1. Transaction Fees

Charging a small percentage or flat fee for each transaction is one of the most common revenue streams for eWallets.

How It Works:

- Fees can apply to peer-to-peer (P2P) payments, bill payments, or merchant transactions.

- Different rates can be set for domestic and international transactions.

Example: PayPal charges 2.9% + $0.30 per transaction for merchants.

Best For: Platforms targeting businesses or users making frequent transactions.

2. Subscription Plans

Offer premium features and charge users or businesses a subscription fee.

Features to Include:

- Faster transaction processing.

- Advanced analytics and spending insights.

- Access to higher transaction limits.

Example: Venmo offers a “Venmo Plus” plan for additional benefits.

Best For: eWallets with advanced functionalities or B2B features.

3. Partner Commissions

Collaborate with merchants and service providers, earning a commission for every transaction processed through your platform.

How It Works:

- Partner with e-commerce platforms, utility providers, and retailers.

- Earn a percentage of the total transaction value as commission.

Example: Alipay earns significant revenue by partnering with local merchants in China.

Best For: Platforms with a large user base and diverse partnerships.

4. Advertisements and Promotions

Generate revenue by allowing businesses to promote their products or services on your platform.

Ad Formats:

- In-app ads for local and global businesses.

- Sponsored content or placement on the homepage.

Example: Google Pay features sponsored offers and cashback deals from partnered brands.

Best For: Platforms with high daily active users (DAU).

5. Cross-Selling Financial Services

Expand your offerings by integrating additional financial services such as:

- Personal loans.

- Insurance products.

- Investment tools (e.g., cryptocurrency or stock trading).

Example: Cash App generates revenue by allowing users to trade Bitcoin and invest in stocks.

Best For: Platforms targeting tech-savvy or financially active users.

6. Data Monetization

Analyze user behavior and offer insights (anonymized) to businesses and advertisers.

How It Works:

- Provide anonymized spending patterns to help businesses improve their strategies.

- Use analytics to create detailed consumer profiles for targeted advertising.

Tip: Always adhere to privacy laws like GDPR or CCPA to avoid legal issues.

Best For: Platforms with large, active user bases and a focus on compliance.

7. Referral Programs

Earn revenue by referring users to partner platforms or services.

How It Works:

- Partner with service providers (e.g., streaming platforms or travel agencies).

- Offer users discounts or perks while earning referral commissions.

Example: Some eWallets partner with credit card companies to promote specific cards.

Best For: Platforms with a focus on lifestyle and value-added services.

8. White-Label Solutions

License your eWallet technology to other businesses looking to offer similar services.

How It Works:

- Develop a customizable solution that other businesses can rebrand and deploy.

- Charge a one-time licensing fee or ongoing subscription for usage.

Example: Many smaller eWallets use white-labeled versions of existing technologies.

Best For: Established eWallets with robust technology infrastructure.

Estimating Revenue Potential

Your revenue depends on the size of your user base, average transaction value, and monetization strategies.

Example Calculation:

- User Base: 100,000 users.

- Average Transactions per User: 10 per month.

- Transaction Fee: $0.50 per transaction.

Monthly Revenue = 100,000 × 10 × $0.50 = $500,000.

Combining multiple revenue streams can maximize your profitability. Start with transaction fees and partner commissions, then scale with ads, subscriptions, or financial services as your platform grows.

Partner with eBizneeds: Your Trusted eWallet App Development Company

Building a successful eWallet platform requires expertise, innovation, and a commitment to quality.

That’s where eBizneeds comes in.

With years of experience in delivering robust, scalable, and secure eWallet solutions, we’re here to help you turn your vision into reality.

That’s what makes us a leading eWallet app development company.

- Customized Solutions: Tailored eWallet development services that align with your business goals.

- Cutting-Edge Technology: Expertise in blockchain, AI, and multi-currency support to keep you ahead of the curve.

- Regulatory Compliance: Comprehensive knowledge of global compliance requirements to ensure a smooth launch.

- Seamless User Experience: UI/UX designs that prioritize user satisfaction and retention.

Ready to create an eWallet platform that stands out? Partner with eBizneeds and start your journey today!

Conclusion

Starting an eWallet business is your gateway to entering a lucrative and rapidly growing industry. From preparation to launch, and even scaling, each step requires meticulous planning and execution. By understanding the market, leveraging innovative features, and addressing potential challenges, you can build a platform that stands out.

With a focus on user trust, regulatory compliance, and an intuitive user experience, your eWallet can attract a loyal user base and create long-term revenue streams. Remember, success doesn’t come overnight-it requires continuous improvement and adapting to market trends. Whether you’re a budding entrepreneur or an established business looking to venture into the fintech space, the right strategy and partners can make all the difference.

FAQs

To start an eWallet business, you’ll need to research the market, secure necessary licenses, develop the platform, and launch with a strategic marketing plan. Partnering with an experienced development team like eBizneeds can simplify the process.

The cost varies based on features, technology, and scale but typically ranges from $50,000 to $250,000 or more. Starting with an MVP can help reduce initial expenses.

You can earn revenue through transaction fees, subscription plans, partner commissions, advertisements, and offering additional services like loans or cryptocurrency trading.

Common challenges include regulatory compliance, ensuring security, building trust, and achieving scalability. Addressing these proactively is essential for success.

Development timelines depend on the complexity and features of the app. A basic eWallet can take 4–6 months, while more advanced platforms may take up to a year.

Naveen Khanna is the CEO of eBizneeds, a company renowned for its bespoke web and mobile app development. By delivering high-end modern solutions all over the globe, Naveen takes pleasure in sharing his rich experiences and views on emerging technological trends. He has worked in many domains, from education, entertainment, banking, manufacturing, healthcare, and real estate, sharing rich experience in delivering innovative solutions.