Picture this: no more fumbling for cash or cards. A quick tap on your phone, and your payment is done.

That’s the power of eWallets. And in Europe, they’re changing the way people handle money.

With the shift towards cashless payments, the eWallet market is booming. From online shopping to splitting bills, people now prefer fast, secure, and hassle-free options.

For entrepreneurs, this is an exciting chance. Europe’s fintech-friendly environment, strong digital adoption, and supportive regulations make it the perfect place to start.

In this blog, you’ll learn how to start an eWallet business in Europe step by step. Let’s get started!

Why Start an eWallet Business in Europe?

The European market is a thriving hub for digital payments, making it the ideal place to launch an eWallet business.

Here’s why:

High Smartphone Penetration

Europe has one of the highest smartphone usage rates in the world.

Countries like the UK, Germany, and the Netherlands boast over 90% smartphone penetration.

This widespread access to mobile technology ensures a ready audience for eWallet platforms.

Whether for online shopping or quick in-store payments, consumers are looking for mobile-friendly solutions.

Cashless Economy on the Rise

Several European nations are rapidly transitioning to cashless economies.

Sweden, for example, is leading the charge, with only 9% of transactions made using cash.

Other countries, like Denmark and Norway, are following close behind.

This shift creates a massive demand for eWallets to facilitate everyday payments seamlessly.

Favorable Regulatory Framework

Europe has implemented progressive fintech regulations, such as the PSD2 (Payment Services Directive 2).

This regulation encourages innovation by enabling third-party providers to offer financial services, ensuring a secure and competitive digital payments landscape.

As an eWallet startup, you can leverage these policies to create cutting-edge solutions.

Diverse and Growing Market

Europe’s 44 countries offer a unique mix of established markets and emerging economies.

While Western Europe provides a strong foundation with tech-savvy users, Eastern Europe represents untapped potential for eWallet adoption.

This diversity allows you to target a wide range of customer needs with tailored solutions.

Fintech Boom in Major Cities

European cities like London, Berlin, and Amsterdam are fintech hotspots.

They attract top talent, investment opportunities, and partnerships that can accelerate your eWallet business.

With such an ecosystem, launching and scaling a startup becomes far more accessible.

The combination of a tech-savvy population, cashless adoption, and supportive policies makes Europe the perfect playground for eWallet entrepreneurs.

Understanding the Different Forms of eWallet Businesses

To launch a successful eWallet business in Europe, it’s important to choose the right model that suits your target audience and business objectives.

eWallets come in various forms, each offering unique benefits and use cases.

Let’s dive into the details.

1. Closed eWallets

A closed eWallet is designed exclusively for use within a specific company or its services.

Users cannot transact outside the platform.

These wallets are typically used to enhance customer loyalty and simplify payments within a business’s ecosystem.

- Example: A travel booking platform like Ryanair might offer an eWallet for flight bookings, where users can deposit money and use it for purchases only on their app or website.

- Advantages:

- Encourages repeat transactions within your ecosystem.

- Reduces payment failures as users preload funds into the wallet.

- Easier to implement since it has limited external integrations.

- Challenges:

- Limited usability might deter customers from adopting the wallet.

- Needs high brand loyalty to succeed.

2. Semi-Closed eWallets

Semi-closed eWallets strike a balance between flexibility and control.

They allow users to transact at partnered merchants or service providers, both online and offline.

- Example: A wallet like Sodexo or Paytm (in certain regions) enables users to shop at specific partner outlets, pay bills, or recharge services.

- Advantages:

- Provides more utility than closed wallets, attracting more users.

- Builds partnerships with merchants, boosting ecosystem growth.

- Ideal for industries like food delivery, retail, and entertainment.

- Challenges:

- Requires constant collaboration with merchants for seamless integration.

- Managing partnerships and keeping users engaged can be complex.

3. Open eWallets

Open eWallets are the most versatile and widely used type.

They allow users to make payments at any merchant, transfer funds, and even withdraw cash from ATMs.

These wallets are often linked to a user’s bank account or card for added functionality.

- Example: PayPal, Google Pay, and Apple Pay are leading examples of open eWallets.

- Advantages:

- High user convenience as they work almost anywhere.

- Attracts a broad audience, including individual consumers and businesses.

- Supports features like bank transfers, cashback, and bill payments.

- Challenges:

- Requires complex security measures to protect user data.

- Regulatory compliance is stricter due to the involvement of financial institutions.

4. Cryptocurrency Wallets

With the rise of blockchain technology, cryptocurrency wallets are gaining significant traction in Europe.

These wallets are used for storing, transferring, and trading cryptocurrencies like Bitcoin, Ethereum, and others.

- Example: Binance Wallet and Coinbase Wallet are popular choices in the crypto market.

- Advantages:

- Appeals to tech-savvy users and investors interested in digital assets.

- Adds an innovative edge to your eWallet platform.

- Opens opportunities to integrate blockchain-based loyalty programs or tokens.

- Challenges:

- Requires extensive knowledge of blockchain and crypto regulations in Europe.

- Limited adoption among the general public compared to traditional eWallets.

5. Peer-to-Peer (P2P) Payment Wallets

P2P wallets are built for direct money transfers between individuals.

These wallets are widely used for splitting bills, sending small payments, or paying for informal services.

- Example: Venmo and Revolut are popular P2P wallets in Europe.

- Advantages:

- Simplifies everyday transactions like splitting dinner bills or paying rent.

- Easy to use, making them highly appealing to younger audiences.

- Can integrate social features like transaction comments or payment history sharing.

- Challenges:

- Limited to personal transactions unless combined with other wallet features.

- Monetization is more challenging due to the small transaction amounts.

6. Multi-Currency Wallets

Multi-currency wallets are designed to facilitate payments and money transfers in multiple currencies, making them ideal for international transactions.

- Example: Wise (formerly TransferWise) allows users to hold, transfer, and exchange various currencies with ease.

- Advantages:

- Perfect for businesses and travelers who need cross-border payments.

- Attracts a global audience, expanding your market reach.

- Supports currency conversions at competitive rates.

- Challenges:

- Requires compliance with cross-border payment regulations.

- Complex infrastructure to support multiple currencies securely.

7. Niche-Specific Wallets

These are eWallets tailored to serve a specific industry or purpose.

Examples include wallets for ride-hailing apps, gaming platforms, or healthcare services.

- Example: Uber Wallet for managing ride payments or Steam Wallet for purchasing games.

- Advantages:

- Highly focused, offering a seamless experience for the target audience.

- Can include industry-specific features like rewards, credits, or prepaid packages.

- Challenges:

- Limited scalability unless the wallet expands beyond its niche.

- Heavy reliance on the success of the specific industry or platform.

Understanding these eWallet types helps you identify which model aligns best with your business goals.

Whether you aim to target everyday consumers, tech-savvy crypto users, or international travelers, choosing the right form of eWallet is the first step towards building a successful platform in Europe.

What Makes Europe a Great Place to Start an eWallet Business?

Europe isn’t just another market, it’s a thriving fintech hub with unique advantages for eWallet startups.

Let’s explore the key reasons why Europe stands out as the perfect place to launch your eWallet business.

1. Cashless Trends Are Growing Rapidly

European countries are leading the global shift towards cashless payments.

Nations like Sweden, where cash usage is below 10%, and Norway, with similar trends, show a strong demand for digital payment solutions.

In major cities like Stockholm, Amsterdam, and Copenhagen, businesses have fully embraced cashless transactions.

This creates a fertile ground for eWallet adoption.

2. Supportive Regulatory Framework

Europe’s regulatory environment is designed to foster innovation in fintech.

The Payment Services Directive 2 (PSD2) encourages open banking, allowing third-party providers to create innovative payment solutions.

GDPR regulations also ensure consumer data protection, boosting user trust in digital platforms.

Starting an eWallet business in Europe means benefiting from these progressive policies.

3. High Digital Literacy and Smartphone Penetration

Europe boasts some of the highest rates of smartphone penetration, with countries like the UK, Germany, and France leading the charge.

Additionally, digital literacy levels are high across the continent, ensuring that users are comfortable adopting new technologies like eWallets.

Cities like Berlin, London, and Paris are hotspots for tech-savvy consumers who are ready to embrace digital wallets.

4. Diverse and Dynamic Market

With 44 countries and over 750 million residents, Europe offers a diverse and dynamic market.

The region’s mix of developed markets (e.g., Germany, France) and emerging economies (e.g., Poland, Hungary) allows startups to target both mature users and untapped audiences.

This diversity provides endless opportunities to create tailored eWallet solutions for different user groups.

5. Thriving Fintech Ecosystem

Europe is home to some of the world’s top fintech hubs, including London, Amsterdam, and Zurich.

These cities provide access to venture capital, cutting-edge tech infrastructure, and talented developers.

The thriving fintech scene means you can collaborate with industry experts and accelerate your business growth.

6. International Appeal and Tourism

Europe is one of the most visited regions globally, with millions of tourists traveling across cities like Rome, Barcelona, and Prague.

An eWallet that offers seamless multi-currency support and international usability can attract both locals and travelers, increasing its adoption and profitability.

7. Strong Consumer Trust in Digital Platforms

European consumers trust digital platforms, particularly those with robust security features.

Fintech adoption is already widespread, with a growing number of users embracing online banking and mobile payments.

By offering a secure and reliable eWallet, you can tap into this trust and build a loyal customer base.

From advanced regulations to a digitally savvy population, Europe offers everything you need to succeed in the eWallet space.

Whether targeting individual consumers, businesses, or tourists, the opportunities in this market are vast and varied.

Step 1: Laying the Foundation – A Checklist to Start an eWallet Business

Starting an eWallet business requires careful planning and preparation.

Before you dive into product development, it’s essential to lay a solid foundation.

Here’s a checklist to guide you through the initial steps:

1. Identify Your Target Audience

Understanding your audience is key to designing an eWallet that meets their needs. Are you targeting:

- Everyday consumers for quick and secure payments?

- Small businesses looking for easy transaction management?

- International travelers needing multi-currency support?

Research your audience’s pain points and preferences to craft a solution that fits.

2. Conduct Market Research

Analyze the competition and identify gaps in the European market.

Study successful eWallet platforms like PayPal, Revolut, and Wise.

Look for opportunities to introduce innovative features or target underserved regions.

3. Choose the Right Business Model

Decide on the type of eWallet you want to develop: closed, semi-closed, open, or niche-specific.

The business model should align with your goals, whether it’s customer retention, broad usability, or international expansion.

4. Secure Funding

Starting an eWallet business involves significant investment in technology, compliance, and marketing. Consider these funding options:

- Venture capital

- Angel investors

- Government fintech grants

- Crowdfunding platforms

5. Understand Legal and Regulatory Requirements

Europe has strict regulations for digital payments. Ensure compliance with:

- PSD2 (Payment Services Directive 2): Enables secure and innovative payment services.

- GDPR (General Data Protection Regulation): Protects user data and privacy.

- Local licensing requirements for operating as a financial service provider in each country.

Consult legal experts to navigate the regulatory landscape.

6. Define Your Unique Selling Proposition (USP)

What makes your eWallet different? Will it offer enhanced security, multi-currency support, or faster transactions? A strong USP will set your platform apart in a competitive market.

7. Partner with Payment Gateways and Financial Institutions

Collaborating with banks, financial institutions, and payment gateways is crucial. They provide the infrastructure for secure transactions, currency exchanges, and cross-border payments.

8. Draft a Business Plan

Create a detailed business plan outlining:

- Goals and objectives

- Financial projections

- Marketing strategies

- Revenue model

A solid business plan will attract investors and keep your team aligned.

9. Build a Strong Team

Your team should include:

- Experienced developers for platform creation.

- Legal advisors to ensure compliance.

- Marketing experts to promote your eWallet.

- Customer support staff to assist users.

10. Invest in Security Measures

Security is non-negotiable in the eWallet industry. Implement strong measures like:

- Multi-factor authentication (MFA).

- End-to-end encryption.

- Fraud detection systems.

By following this checklist, you’ll ensure your eWallet business has a strong foundation before moving to the next phase: product development.

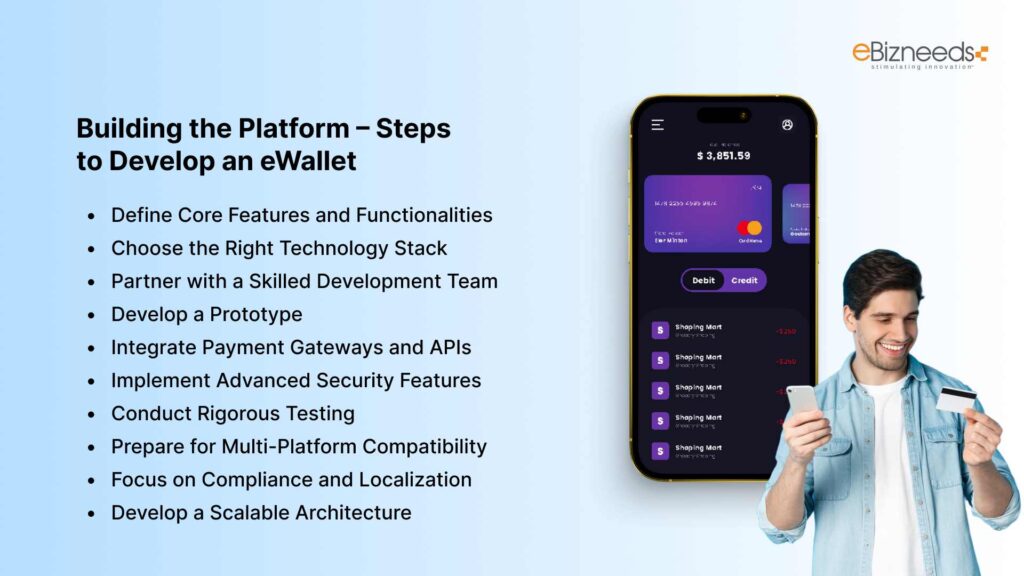

Step 2: Building the Platform – Steps to Develop an eWallet

Once your preparation is complete, it’s time to move to the most crucial phase, developing your eWallet platform.

A robust and user-friendly platform is the backbone of your business.

Let’s break down the ewallet development process step by step.

1. Define Core Features and Functionalities

Your eWallet must offer features that meet user expectations while standing out from the competition.

Here are the essential features to include:

- User Registration and Login: Simple onboarding with email, phone, or social media integration.

- Multi-Currency Support: Essential for cross-border payments and attracting international users.

- Payment Methods: Integration with credit cards, bank accounts, and QR code payments.

- Transaction History: Detailed logs for transparency and user trust.

- Advanced Security: Features like biometric authentication, OTPs, and fraud detection.

- Customer Support: In-app chatbots or help centers for resolving issues quickly.

Consider adding unique features, like AI-driven budgeting tools or cryptocurrency integration, to differentiate your platform.

2. Choose the Right Technology Stack

The technology stack you choose will impact your platform’s performance, scalability, and security.

Some recommendations include:

- Frontend: React.js or Angular for an interactive user interface.

- Backend: Node.js, Django, or Ruby on Rails for fast and scalable server-side processing.

- Database: MySQL or MongoDB for secure data storage.

- Payment Gateways: Stripe, PayPal, or Razorpay for processing payments.

- Cloud Services: AWS or Google Cloud for reliable and scalable hosting.

3. Partner with a Skilled Development Team

Hire a development team with expertise in fintech solutions. This team should include:

- UI/UX designers to create a user-friendly interface.

- Backend developers for secure and efficient functionality.

- Quality assurance (QA) testers to ensure a bug-free product.

- DevOps engineers to manage deployment and maintenance.

4. Develop a Prototype

Start with a minimum viable product (MVP) to test your concept in the market.

An MVP includes only the essential features, allowing you to gather user feedback and make improvements without heavy investment.

5. Integrate Payment Gateways and APIs

Secure and efficient payment processing is the heart of any eWallet. Partner with trusted payment gateways and use APIs for:

- Real-time transaction tracking.

- Currency conversions.

- Linking bank accounts and credit cards.

6. Implement Advanced Security Features

Security should be a top priority during development. Use these measures to protect user data:

- End-to-End Encryption: Ensures that data remains secure during transmission.

- Tokenization: Replaces sensitive data with unique identifiers.

- PCI DSS Compliance: Follows international payment security standards.

7. Conduct Rigorous Testing

Before launching, test your platform extensively. Focus on:

- Functional Testing: Ensures all features work as intended.

- Performance Testing: Evaluates the app’s speed, scalability, and stability.

- Security Testing: Identifies and fixes vulnerabilities.

- Usability Testing: Collects feedback from real users for further refinement.

8. Prepare for Multi-Platform Compatibility

Ensure your eWallet is available on multiple platforms to maximize its reach:

- Mobile App: For iOS and Android users.

- Web Version: For users who prefer browser-based access.

- Wearables: Consider smartwatch compatibility for the tech-savvy audience.

9. Focus on Compliance and Localization

Adapt your platform to meet regional regulations and user needs across Europe:

- Ensure compliance with PSD2 and GDPR.

- Localize languages and currencies for different European countries.

- Customize your platform to suit cultural preferences.

10. Develop a Scalable Architecture

As your user base grows, your platform should scale seamlessly. Use microservices architecture and cloud hosting solutions to handle increasing traffic and transactions.

Building an eWallet requires attention to detail and collaboration with skilled professionals.

Once your platform is ready, you’ll be prepared to move to the next step, launching your business.

Step 3: Launching Your eWallet Business

After successfully developing your eWallet platform, the next critical step is launching it.

A strategic and well-planned launch will help you capture attention, attract users, and create a solid market presence.

Here’s how you can launch your eWallet business effectively:

1. Create a Pre-Launch Buzz

Start building anticipation for your eWallet before the official launch. Use the following strategies:

- Social Media Marketing: Share teasers, videos, and infographics on platforms like Instagram, LinkedIn, and Twitter.

- Email Campaigns: Reach out to your target audience with sneak peeks and exclusive offers for early adopters.

- Influencer Collaboration: Partner with influencers in the fintech and technology space to spread the word.

2. Launch a Beta Version

A beta launch allows you to test your platform with a small group of users before the full rollout. Benefits include:

- Gathering valuable feedback for improvements.

- Identifying and fixing any bugs or glitches.

- Building trust and excitement among early users.

Offer rewards or incentives, such as free credits, to encourage participation.

3. Design an Eye-Catching Marketing Campaign

The success of your eWallet launch largely depends on your marketing efforts. Focus on:

- Highlighting Your USP: Clearly communicate what makes your eWallet unique, be it faster transactions, advanced security, or multi-currency support.

- Targeting Specific Regions: Tailor your campaigns to specific European cities, such as London, Berlin, or Amsterdam, to maximize local engagement.

- Utilizing Paid Ads: Invest in Google Ads and social media ads to reach a broader audience.

4. Offer Launch Incentives

To attract your first wave of users, provide irresistible incentives, such as:

- Signup bonuses.

- Cashback offers on initial transactions.

- Discounts on partnered merchant services.

These incentives encourage users to try your eWallet and create a positive first impression.

5. Partner with Merchants and Businesses

Collaborate with local merchants, online stores, and service providers to increase usability. The more options users have to spend or transfer money, the more likely they are to adopt your eWallet.

6. Ensure a Smooth Onboarding Process

The onboarding experience can make or break your launch. Simplify the process by:

- Offering quick registration with minimal steps.

- Providing an easy-to-navigate interface.

- Including in-app tutorials or guides to familiarize users with the features.

7. Launch with Strong Customer Support

Be prepared to assist users during the launch phase. Common options include:

- In-app live chat or chatbots.

- A detailed FAQ section.

- 24/7 customer support via email or phone.

Good support fosters trust and keeps users engaged.

8. Monitor Performance and Gather Feedback

After launching, closely monitor your platform’s performance. Use analytics tools to track:

- User engagement.

- Transaction volumes.

- Any technical issues.

Simultaneously, gather feedback from users to identify areas for improvement and future updates.

Launching your eWallet business is an exciting milestone, but it’s only the start of your journey. Consistent marketing, feature updates, and excellent user support will ensure long-term success and growth.

Compliances to Keep in Mind When Starting an eWallet Business in Europe

The table below outlines the key compliance requirements for launching an eWallet business in Europe. These regulations ensure secure operations, user trust, and legal adherence:

| Compliance | Description | Key Requirements |

| PSD2 (Payment Services Directive 2) | European directive for safer and more competitive payment systems. | – Strong Customer Authentication (SCA).- Enable open banking through APIs.- Transparent fee structures. |

| GDPR (General Data Protection Regulation) | Protects user data and ensures privacy in digital services. | – Secure collection and processing of personal data.- Obtain explicit user consent.- Provide data management options. |

| Anti-Money Laundering (AML) | Prevents financial crimes such as money laundering and fraud. | – Verify identities through KYC.- Monitor suspicious transactions.- Keep detailed transaction records. |

| Electronic Money Institution (EMI) Licensing | Required to operate legally as an eWallet provider in Europe. | – Obtain an EMI license from local financial authorities.- Maintain minimum capital requirements.- Submit a business plan. |

| PCI DSS (Payment Card Industry Data Security Standard) | Ensures secure handling of payment card data during transactions. | – Encrypt sensitive payment data.- Regularly test security systems.- Restrict data access to authorized personnel. |

| Cross-Border Payment Regulations (SEPA) | Facilitates smooth cross-border transactions within the EU in euros. | – Ensure compatibility with SEPA standards for euro payments.- Enable seamless transactions across EU nations. |

| Tax Compliance | Ensures adherence to VAT and other applicable tax regulations for eWallet transactions. | – Consult tax advisors for country-specific requirements.- Properly document and report taxable transactions. |

| Consumer Protection Laws | Safeguards user rights and ensures transparency in digital services. | – Provide clear terms and conditions.- Offer secure refunds and dispute resolutions.- Be transparent about fees. |

| Cybersecurity Regulations | Protects financial and personal data from breaches and attacks. | – Implement firewalls and encryption.- Conduct regular vulnerability assessments.- Maintain strong cybersecurity protocols. |

Adhering to these regulations not only avoids legal penalties but also builds trust with your users. Compliance is a cornerstone of sustainable growth in the eWallet industry.

Challenges You Might Face & Their Solutions

Starting an eWallet business in Europe is exciting, but it comes with its own set of challenges. Here are some common hurdles and practical solutions to overcome them:

| Challenge | Description | Solution |

| Regulatory Complexity | Navigating Europe’s strict financial regulations like PSD2, GDPR, and AML can be daunting. | – Hire legal experts to ensure compliance.- Use pre-built regulatory compliance tools and APIs. |

| Building User Trust | Users may hesitate to adopt new eWallets due to security concerns or lack of familiarity. | – Invest in strong security measures (encryption, MFA).- Highlight certifications and compliance in marketing. |

| High Competition | Competing with established players like PayPal, Google Pay, and Revolut can be challenging. | – Focus on a unique selling proposition (e.g., niche market, innovative features).- Offer launch incentives like cashback. |

| Cross-Border Payment Integration | Supporting multi-currency and cross-border payments adds technical complexity. | – Partner with experienced payment gateways like Stripe or Wise.- Implement SEPA-compliant systems for euro payments. |

| High Development Costs | Developing a secure and feature-rich platform requires significant investment. | – Start with a Minimum Viable Product (MVP) to control initial costs.- Outsource development to cost-effective regions. |

| Fraud and Security Risks | Fraudulent transactions and data breaches can damage your platform’s reputation. | – Use AI-based fraud detection systems.- Regularly conduct security audits and vulnerability testing. |

| Localization Challenges | Catering to Europe’s diverse languages, cultures, and currencies is complex. | – Offer multi-language support.- Customize features to suit regional preferences.- Ensure multi-currency functionality. |

| Scalability Issues | Scaling your platform to handle a growing user base and transactions can strain infrastructure. | – Use cloud-based hosting solutions like AWS.- Implement a microservices architecture for flexibility. |

| Customer Retention | Attracting users is easier than retaining them in a highly competitive market. | – Introduce loyalty programs, rewards, and gamification features.- Provide exceptional customer support. |

| Technical Challenges | Ensuring seamless integration of APIs, payment gateways, and real-time processing is demanding. | – Work with experienced fintech developers.- Use reliable APIs and third-party integrations. |

Every challenge is an opportunity to refine your eWallet business and stand out in the market.

With careful planning, innovative solutions, and the right partnerships, you can address these challenges effectively.

Popular eWallet Businesses & Their Success Stories

Understanding the strategies of successful eWallet platforms can guide your journey in building a thriving business.

Let’s explore some of the most popular eWallet businesses in Europe and what makes them standout.

PayPal

As one of the pioneers in digital payments, PayPal has built a reputation as a global leader.

Its success lies in its ease of use, robust security, and international payment capabilities.

PayPal’s buyer protection feature has made it a trusted choice for online shoppers and businesses alike.

Revolut

This UK-based fintech giant is a game-changer in the eWallet and digital banking space, with over 30 million users globally.

Revolut stands out for its multi-currency accounts, cryptocurrency trading features, and budgeting tools, making it a favorite among tech-savvy users.

Wise (formerly TransferWise)

Wise is renowned for offering transparent and affordable international money transfers.

Its multi-currency eWallet appeals to travelers and businesses that deal with cross-border transactions, thanks to its competitive exchange rates and seamless borderless accounts.

Apple Pay

Integrated with Apple devices, Apple Pay has become a household name across Europe.

Its contactless payment capabilities, biometric authentication, and seamless in-app purchase experience have cemented its position as a reliable and user-friendly eWallet solution.

Google Pay

With a simple interface and widespread merchant network, Google Pay is one of the most widely adopted eWallets in Europe.

Features like secure tokenization, quick payments, and loyalty card integration make it a favorite for both users and businesses.

Klarna

This Swedish eWallet platform has revolutionized eCommerce with its “buy now, pay later” services.

Klarna’s flexible payment options, interest-free installments, and in-app shopping experience have made it a hit among online shoppers.

Skrill

Skrill is known for its secure online payment and money transfer capabilities.

With cryptocurrency support, low transaction fees, and a prepaid Mastercard option, Skrill has carved a niche for itself in the European fintech market.

Venmo

Venmo’s peer-to-peer payment platform is gaining traction in Europe due to its social features.

Users can add transaction notes, share payments with friends, and instantly transfer funds to bank accounts, making it a fun and practical solution.

N26

Berlin-based N26 is more than just an eWallet, it’s a digital bank.

Its real-time notifications, financial analytics, and ATM withdrawal options have made it a popular choice for users seeking modern banking features combined with eWallet functionality.

Zettle by PayPal

Targeted at small businesses, Zettle combines mobile point-of-sale systems with eWallet capabilities.

Its easy payment tracking, business analytics, and hardware integration make it an ideal solution for entrepreneurs and local merchants.

These success stories highlight the importance of innovation, user focus, and trust-building in creating a competitive eWallet platform.

How Much Does It Cost to Start an eWallet Business?

The cost of starting an eWallet business in Europe can vary significantly depending on your business model, features, and target audience.

However, understanding the major cost components can help you plan your budget effectively.

Here’s a detailed breakdown of the key expenses:

1. Platform Development Costs

Developing an eWallet platform is the largest investment. Costs depend on the complexity of features and the technology stack you choose.

- Basic eWallet (MVP): €30,000–€50,000

- Advanced eWallet with multi-currency and security features: €80,000–€150,000

Hiring a skilled development team or outsourcing to a reliable app development company significantly impacts these costs.

2. Licensing and Compliance Costs

Operating in Europe requires compliance with regulations like PSD2, GDPR, and AML, as well as obtaining an Electronic Money Institution (EMI) license.

- EMI license application: €10,000–€50,000

- Regulatory consultancy fees: €5,000–€20,000

3. Payment Gateway Integration

Integrating secure payment gateways and APIs for bank account linking and real-time processing comes at a price.

- Gateway integration: €5,000–€15,000 (per gateway)

4. Security Measures

Implementing advanced security features is crucial for user trust and regulatory compliance.

- Encryption and fraud detection systems: €10,000–€30,000

- PCI DSS compliance: €5,000–€10,000

5. Infrastructure Costs

You’ll need cloud hosting and scalable architecture to handle growing transactions and users.

- Cloud services (AWS, Google Cloud): €1,000–€5,000 per month

6. Marketing and Promotion

Launching and promoting your eWallet requires strategic marketing campaigns to attract users.

- Pre-launch campaigns: €5,000–€20,000

- Social media and paid ads: €2,000–€10,000 per month

7. Customer Support Setup

Providing excellent customer support is vital for user retention.

- In-app chatbots and support tools: €3,000–€8,000

- Customer support team: €2,000–€5,000 per month

8. Maintenance and Updates

Regular updates and maintenance are necessary to ensure your eWallet runs smoothly and stays competitive.

- Ongoing maintenance: €5,000–€15,000 per month

Estimated Total Cost

Based on these factors, the approximate cost to start an eWallet business in Europe is:

- Basic eWallet (MVP): €70,000–€100,000

- Advanced eWallet: €150,000–€300,000

Starting with an MVP can help you reduce upfront costs and test your business idea. Partnering with an experienced app development company can also optimize development and compliance expenses.

Driving Revenue Through eWallet Business: Monetization Methods

Monetization is the backbone of any successful eWallet business.

By implementing effective revenue strategies, you can ensure long-term profitability and growth.

Here are some proven methods to drive revenue through your eWallet platform:

1. Transaction Fees

Charging a small fee for each transaction is one of the most common monetization methods.

- How It Works: Apply fees on transactions like money transfers, bill payments, or purchases.

- Example: PayPal charges a percentage-based fee on every business transaction.

- Potential: This model works well if your platform handles high transaction volumes.

2. Subscription Plans

Offer premium plans for users or businesses who require advanced features.

- How It Works: Provide features like higher transaction limits, multi-currency accounts, or advanced analytics for a monthly or annual fee.

- Example: Revolut offers tiered subscription plans with exclusive perks.

- Potential: Subscriptions ensure recurring revenue, making it easier to predict cash flow.

3. Interchange Fees

Earn a portion of the fees charged by card networks (like Visa or Mastercard) on transactions made through your platform.

- How It Works: Partner with card networks and earn a small percentage from every transaction made using linked debit or credit cards.

- Example: Apple Pay earns interchange fees from its partnerships with card issuers.

- Potential: This model is ideal for platforms with significant card payment activity.

4. Merchant Commissions

Collaborate with merchants and charge a commission on every sale made through your eWallet.

- How It Works: Partner with retailers, restaurants, and service providers who use your platform for payments.

- Example: Google Pay charges merchants a percentage of each transaction.

- Potential: Works well in industries like eCommerce, travel, and food delivery.

5. Advertisement Revenue

Leverage your platform to display targeted ads and promotions from merchants or businesses.

- How It Works: Offer ad space in your app or send targeted promotions to users based on their spending habits.

- Example: eWallets like Venmo display sponsored offers from brands.

- Potential: Provides an additional revenue stream while engaging users with relevant offers.

6. Data Insights and Analytics

Offer anonymized spending data and insights to businesses for market research.

- How It Works: Provide aggregated data to businesses about user spending trends or preferences.

- Example: Many fintech companies monetize insights while ensuring user privacy (GDPR compliance).

- Potential: Works well for B2B partnerships, especially with retailers and advertisers.

7. Cross-Border Payments and Currency Exchange Fees

Charge fees for international transfers or currency conversions.

- How It Works: Provide cross-border payment services and earn from exchange rate margins or transfer fees.

- Example: Wise (TransferWise) charges low but competitive fees for currency exchanges.

- Potential: High profitability if your platform supports multi-currency accounts.

8. Partnered Loyalty Programs

Collaborate with businesses to offer exclusive loyalty programs to users.

- How It Works: Earn commissions from businesses for driving customer engagement through loyalty points or cashback.

- Example: eWallets like Paytm partner with brands to reward customers for transactions.

- Potential: Helps retain users while generating revenue from merchant collaborations.

eBizneeds – Your Trusted Partner for eWallet App Development

Building an eWallet business in Europe is a promising endeavor, but it requires the right expertise to turn your vision into a secure, scalable, and feature-rich platform.

That’s where eBizneeds comes in.

As a leading eWallet app development company, we specialize in creating tailored eWallet solutions that meet your business needs while adhering to Europe’s strict compliance and regulatory standards.

Whether you’re starting with an MVP or aiming to launch a full-fledged eWallet with advanced features, we have the experience and expertise to deliver

Conclusion

Starting an eWallet business in Europe is an exciting opportunity in today’s thriving fintech market. With the growing demand for cashless transactions, a tech-savvy population, and a supportive regulatory environment, Europe offers the perfect setting to launch your eWallet platform.

From choosing the right business model to understanding compliance requirements, every step plays a crucial role in building a successful eWallet. By offering innovative features, focusing on user security, and implementing effective monetization strategies, you can create a platform that not only attracts users but also drives consistent revenue.

Remember, challenges like regulatory complexities and fierce competition can be tackled with the right approach, strong partnerships, and expert guidance. By following the steps outlined in this guide, you’re already on the path to transforming your eWallet idea into a thriving business.

The future of payments is digital, are you ready to make your mark in Europe’s booming eWallet market?

FAQs

The cost can range from €70,000 for a basic MVP to €300,000 for a fully-featured advanced platform, depending on development, compliance, and marketing requirements.

Compliances include PSD2, GDPR, AML regulations, PCI DSS, EMI licensing, and SEPA compatibility for cross-border payments.

You can monetize through transaction fees, subscription plans, merchant commissions, currency exchange fees, advertising, and loyalty programs.

Key features include secure user registration, multi-currency support, transaction history, payment integration, advanced security, and customer support.

Developing an eWallet can take 4–12 months, depending on the platform’s complexity, features, and compliance requirements.

Europe’s cashless trends, high digital adoption, fintech-friendly regulations, and diverse market opportunities make it an ideal region to launch an eWallet.

Udai Singh Shekhawat is the SEO Content Strategist and team lead at eBizneeds, with deep expertise in fintech and eWallet app development. He crafts result-oriented content strategies tailored for Western and Australian markets, driving impactful brand engagement and user acquisition through innovative storytelling and industry-specific insights.